Higher rate pension tax relief

Discover the ins and outs of higher rate pension tax relief.

Key points:

- Pension tax relief adds government‑funded top‑ups to personal pension contributions as an incentive to save for retirement.

- Higher‑rate taxpayers can claim extra pension tax relief beyond the basic rate when using a Relief at Source scheme.

- In Relief at Source schemes, providers add basic‑rate relief automatically, and members who pay tax at a higher rate claim the relief direct from HMRC.

- If you've missed tax relief at a higher rate in previous tax years, you can still claim it direct from the HMRC. They give you four tax years for this.

Part of planning for the future means making the most of every contribution you put towards your pension, and understanding how tax relief works is an important part of that.

What is pension tax relief?

Pension tax relief is the money you receive on top of your regular contributions by the government as an incentive for paying into a pension. Please note, tax rules can change and any benefits are dependent on individual circumstances.

There are two bases on which your contributions can receive tax relief:

- net pay arrangement

- Relief at Source (RAS)

Only employer-sponsored schemes who sign up to use it can use the net pay arrangement basis. Personal pensions all use the Relief at Source basis of tax relief.

In a Relief at Source scheme, tax relief at basic rate is claimed by the scheme from HMRC and paid into your pension, as part of your contribution. So, for every £1 you pay in, the government will add 25p.

Employer-sponsored schemes can alternatively use the net pay arrangement to give tax relief on employee (personal) contributions. In this case, your contributions are deducted from your pay before tax is calculated. This means that you get full and immediate tax relief at your highest rate of tax before the contribution reaches the pension scheme.

Find out more about pension tax relief.

The government provide tax relief on payments as an incentive for people to think about their future retirement. By promoting this, the government is aiming for long-term financial security to work alongside the state pension.

What is higher rate pension tax relief

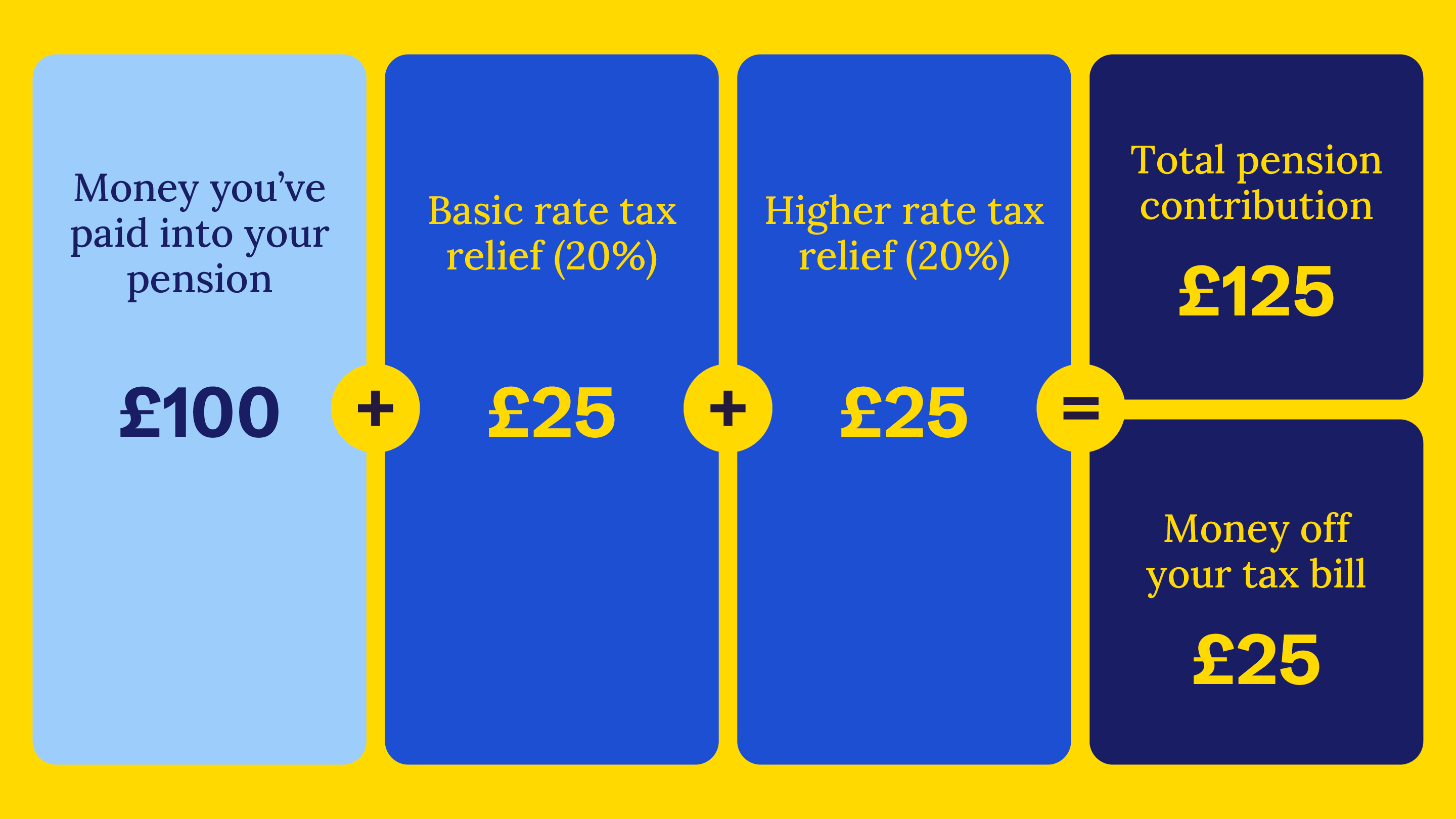

As a higher rate taxpayer in a relief at source scheme, you are entitled to more tax relief than the basic rate. You’re able claim back a further 20% of your payments, so it can look something like this –

The principle is still the same if you pay tax at different rates, such as additional rate in England, Wales and Northern Ireland, and at one or more of the relevant rates in Scotland: you will need to claim the extra part directly. The amount of tax relief that goes into the scheme will be the same, but you will get a different amount of money off your tax bill.

How to claim higher rate tax relief on pension contributions

If you are a higher rate taxpayer, you can claim back a further 20% of your payments, but it’s something you need to do through your self assessment tax return which you must complete yearly with HM Revenue and Customs (HMRC).

Can I claim higher rate tax relief for previous years?

If you have been paying tax at a rate higher than 20% in previous tax years, and paying personal contributions into a Relief at Source scheme, you can claim additional tax relief you've missed out on.

There is a time limit for how many years you can claim back on – you can only revise your self-assessment tax returns for the last four tax years, to claim any additional tax relief you've not yet received.

If someone else pays into my pension, who gets the tax relief?

If the provider agrees, anyone can pay into your pension. But remember - the member gets the tax relief, not the payer. So, if you pay into your child's pension, they get the tax relief, and it doesn't affect the amount of higher or additional rate tax you pay.

If someone else pays into your pension, remember to claim any higher or additional rate tax relief you're due. Also, remember to tell them how much annual allowance you've already used, as you'll be liable for any annual allowance charge due if their contribution means a charge is payable.

What are the pension tax relief rules and limits?

There are two limits when it comes to your pension contributions:

- Your annual allowance – this includes the Money Purchase Annual Allowance or a Tapered Annual Allowance. It measures how much is paid into pensions for your benefit. If that goes over the annual allowance that applies to you, you'll be liable for a tax charge.

- Your relevant UK earnings – this limits the amount of tax relief you can claim on your own contributions based on your income.

Tax relief is available on contributions up to your UK earnings, or £3,600 if your earnings are lower. This includes your tax relief, so it's always worth checking what that could look like. Our pensions can only accept contributions from you or another payer other than your employer that are eligible for tax relief. Your circumstances can change your annual allowance, so if you’re unsure what your annual allowance is you can check on the gov.uk website.

A pension adviser can help provide further support in understanding your options, to help with your retirement planning.

It is important to remember the value of a pension can go down as well as up. You could get back less than invested.

Next article

A guide to an early retirement

Dream your early retirement lifestyle goals and find the steps to reach them with our guide.

Related articles

Get in touch

You can get our expert, personalised advice if you have £300,000 or more in total across all your pension and investment savings. Our Customer Wealth Engagement Team is here to help you explore if financial advice is right for you. Give them a call for a no-fee, no-obligation chat, or book a call back.

Call us on 0800 046 8408

Monday to Friday: 9:00am - 5:00pm

Weekends and bank holidays: Closed